Eric, Ilsa, and Us

Special guest Alexandra Macqueen

Alexandra Macqueen is a Certified Financial Planner, retirement income specialist, co-author of the (soon-to-be) newly revised book Pensionize Your Nest Egg, and very gracious about usually being the smartest and most articulate person in the room (or online forum).

She’s @MoneyGal on Twitter.

This episode is about Eric and Ilsa, the big-hat, no cattle couple from Vancouver who were featured in the Globe and Mail’s Financial Facelift series last week. The couple spawned a Twitter hashtag and parody account, and basically blew up the internet for an entire week for reasons which we get into below.

We also reached out to Dianne Maley, who started the Financial Facelift feature for the Globe back in 1998, to comment about Eric and Ilsa and how the column spiralled out of control. She said the doctor was recognized after the feature was published and so the Globe tried to clarify the situation as much as they could “without adding to his misery”.

Dianne:

“When we wrote the facelift, we had precisely the information we relayed. He worked one day at a clinic and earned so much. True. He worked one day at the university, which naturally spills over, and earned so much. True.

What we should have said is he earns $300,000 a year. That’s enough.

Anyway, he was spending more time on the relatively low paying university job than he could afford. The planner – our most senior — figured Eric could tighten the university work up and work at the clinic another day.

The planner bounced this idea off the doctor and he acknowledged that was a possibility. The planner likes to find solutions. The doctor’s wife, when she saw the published facelift, objected. Working another day was not an option to her.

It never occurred to either of us that we were making the doctor look like he was lazy.”

The senior planner – Warren MacKenzie of HighView Financial Group – had this to say:

“It was an unfortunate situation – the good doctor was careless in providing us with information for the facelift and in reality he is working much harder than the column suggests. In fact, I now understand that he is working 70 to 80 hours per week. Each ‘day’ at the clinic is actually a 17 hour day with considerable follow up required – so it is not practical for him to work another day. That being the case the best solution for him will be to reduce his spending.”

We feel for the couple – truly – and this episode was recorded before we knew many of the above mentioned details. That said, this Because Money episode is not about making fun of Eric and Ilsa, it’s about sound bite financial advice and all the reasons why a column like this can go off the rails. Enjoy:

Transcript

Jackson: Jackson Middleton

Alexandra: Alexandra Macqueen

Robb: Robb Engen

Sandi: Sandi Martin

Jackson: Hey everybody welcome to another episode of the Because Money Podcast. Today we’re talking about Eric and Ilsa, and that’s about all I have to say so, Robb, it’s on to you.

Robb: Thanks Jackson, well Eric and Ilsa, the Financial Facelift article in The Globe and Mail that spawned a hashtag and a parody Twitter account, and countless scorn throughout the blogosphere, I guess. It’s just a quick background.

Pretty much every major newspaper does one of these kind of family profiles where they look at somebody’s financial situation. They have some kind of an issue, they bring in a financial planner and try to solve that issue in 1,000 words or less.

The lowdown on Eric and Ilsa

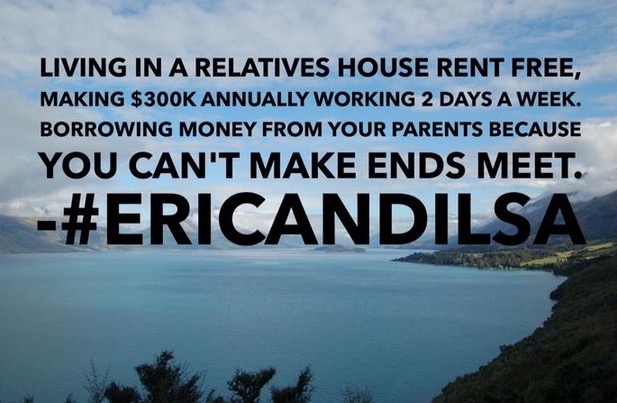

So this one particular Financial Facelift on The Globe and Mail was Eric and Ilsa, and it was so ridiculous. It started out as a doctor who worked one day a week and taught at a university for one day a week. I think he made $300K. His wife was a dentist on maternity leave. They had five children. I think all together they brought in $360K, soon to be $450K a year, and talking about living in a relative’s home, rent free. I believe that house was up for sale or for some reason they needed to get out of that house, so the problem was they couldn’t afford a downpayment. So the argument, or the struggle, was this professional couple, they can’t make ends meet and what do they need to do.

So obviously to many readers the solution was, well you should probably work one more day a week. You’re only working two days a week and one in a clinic, and you could probably make another $50K to $100K doing that, and problem solved. Obviously, there are some spending issues that need to be got under control, but the readers obviously started to point that out.

I don’t know, I’ll kick it over to Sandi. What happened after that, it was just a whole cluster of events that people went crazy over this couple and the shoddy journalism, basically, that ended up happening afterward.

Sandi: Yeah, a cluster is right. Suddenly it turned into, instead of one day a week, in fact he worked 80 hours a week. And instead of $6K a month in professional fees, it was suddenly $6K a year. So that dropped and obviously that changes everything about that Financial Facelift and no longer — the advice which was in the facelift originally was “work an extra day” — now, obviously it’s something completely different. So then the story turned into now he works over 100 hours a week. Anyway, there continued to be kind of these completely different corrections.

Robb: Buried underneath the whole story, right?

Sandi: Yeah, in italics under the story. And then the rhetoric started—all of the funny and ironic comments and the Twitter eye-rolling, but then The Globe and Mail and a bunch of very serious people started chastising everyone. Rob Carrick showed up on the next day with another article–He didn’t write the first one, obviously–but he came out with his own opinion piece which was the mocking Eric and Ilsa is easy, let’s talk about the wealth gap and the 1%, and how we’re all Eric and Ilsa, “you’re just mad that they’re rich”. I think that’s not really the point of what most people were angry about so it’s was just all-round crazy.

Robb: We’re really happy to be joined by Alexandra Macqueen, who has helped out on some of these Financial Facelifts in the past. Welcome Alexandra, and maybe give us your take on this particular story and tell us about how they’ve gone in the past in terms of what kind of details you get from the journalist and from the couple.

Alexandra: Well I think there’s a lot of different places we could go with the whole Financial Facelift phenomenon. Because as you pointed out, The Globe and Mail has been running a Financial Facelift for many, many years, and The Financial Post does one as well.

Robb: Yeah, and The Star does.

Alexandra: The Star does one every week, and MoneySense–you know what, there’s probably others. There are advisor publications that certainly do case studies for people who write in.

So there’s an appetite for this kind of financial advice. Clearly people want it and lots of readers like it. Lots of people say to me and I’ve certainly heard many times that, “This is my favourite part of The Globe and Mail. I love to get it on Saturday morning. It’s the first thing I turn to. It’s so interesting to read.”

So, one question that’s really there for me is why do we like these so much? Why do people seek financial advice out in that forum and why do we, as Canadians, love to read financial advice that’s delivered via these kind of really short snapshots?

Robb: Jackson, let me throw that over to you. What do you, how do you feel about these Financial Facelifts? Are they kind of voyeuristic, do you like diving into this and seeing how this side of the world lives?

Jackson: Well, I don’t really find much value in them, personally. To be quite honest, this is the first one that I’ve actually read from start to finish. And as I was reading it, it was pretty much–my reaction was, “Really? Really? These guys need help with their…?” I was completely blown away. And again, if you read the story that was there before versus reading the story now, you can kind of read this as okay yeah, they need a little bit of help. But I mean as originally written this cat was working one day a week, as a doctor, and one day a week as a professor, making over $300K, and he’s putting his kids in private school, they bought a million dollar house, they’ve got a live-in nanny, and you just kind of go with “Wow, these guys are clowns, they have serious issues. There’s no way. How is this relevant to anyone? This is just straight Globe and Mail getting people to read the paper because it’s outrageous” and that was, I think, the reaction, and I took the bait.

I went to my memes-maker on my phone and I started sharing memes on Twitter. Because why? Because Retweet, I mean, it’s happening. Like it’s just pure gold. And the hashtag #EricandIlsa is just hilarious. I watched somebody today on Twitter say “Oh, I don’t have that kind of money. That’s Eric and Ilsa money.” So I mean, it’s already becoming a thing to make fun of them, but I mean if he’s actually a doctor working 80 hours a week, I don’t begrudge him. Hey, you went to school for 43 years, or however long it is to become a doctor. I’m certainly not going to begrudge you for making the money.

So for me it’s not about the wealth. It’s not about making fun of the 1%. It’s just straight-up, the story had bad facts. So how do I feel about financial facelifts in general? How do I feel about this one? Oh it was fun to roast, but it wasn’t really the truth that we were roasting. So how do I feel about it now? I say we still roast them, because it’s kind of fun.

Truncated, oddly specific financial advice in 800 words or less

Robb: Let’s talk a little bit about the journalism then, because obviously this is a kind sensationalist look at things, and Alexandra, you mentioned that it’s often people’s favourite look into the paper, to dive in to somebody’s finances. So obviously there’s value there from the newspaper side of things. They’re getting eyeballs on these types of articles.

Does The Globe and Mail care that we’re all making fun of this? I noticed that the next day, in Rob Carrick’s column, so on Twitter, The Globe Investor’s saying, here is Rob Carrick’s take on this, and they’re using the hashtag #EricandIlsa. So they’re using this to kind of further along their page views and more eyeballs on their site. You know, Gawker linking to them and just mocking them. Do they care or is it just more eyeballs? They care about the integrity of it, I guess?

Alexandra: Well, I want to speak as somebody who has participated as the planner in two of those columns. So, the first one I did was kind of accidental, and the scenario was very unusual, so it was really not a relatable scenario for most people, but it was a woman at the age of 82. Her situation was very unique. You know, nobody contacted me after that and said, “Wow, this is a relatable story and can you help me out with my finances?” And then they asked me to do another one, which was much more common to kind of an ordinary scenario that a Canadian might find themselves in. It’s professional couple, with a stay-at-home mom. They have two kids to put through university and we want to know can we meet that goal—put them through university and then also retire early?

So I think that’s kind of like the average Canadian Globe and Mail reader’s exact scenario they want advice on. But my thought about the process—you know, I’m no journalist. I provided financial planning advice, but it’s such a truncated little snapshot and yet there’s this very kind of absurd specificity. So it’s like if John and Erica save this much per year and then in 2017 they’ll have $593,300.82. Like it’s very, very bizarrely specific and I have to wonder, do people really read that and get anything from it?

Robb: Yeah, I think they want to read how other people are living right? You all, we all want to peek inside our neighbour’s finances and I hear all these people that are keeping up with the Jones’ and I see the two brand new SUVs and the $0.5M or the $1M house and I want to think that they’re drowning in debt because no one can afford that. And so these kind of give us a little peek inside at that, so maybe we can confirm that, or I don’t know. I don’t know what value is.

Alexandra: I think they tread a line between I think on the readers part, they want the role of the financial planner to be to sweep in and kind of spank the client, “Oh, you’ve done this, and this is not good, and you should do this other thing”. But also the role of the journalist, I think, or the framing of the piece is designed to add kind of relatability and kind of a pleasant wrap-up, like look, here’s their scenario and if they do this one thing, then everything is solved. So there’s this kind of very—I said truncated—but very…you know people often don’t have one issue in isolation that if you solve it, somehow then everything falls into place.

Robb: I think that leads into something that Sandi talked about leading up to this, was about the kind of the sound bite advice. How could you possibly solve somebody’s dilemma in that 800-word column? And I’m going to throw it over to you, Sandi, and talk a little bit about what’s your reaction to these columns and are they helpful? Are they hurting anybody, and what are people actually getting valuable advice out of something that could be again, like you said, truncated down to a column?

Sandi: I think it’s far-fetched to believe that somebody with a similar background–let’s say a stay-at-home mom and two kids to put into university and the desire to retire early, if we use that as an example–it’s far-fetched to believe that someone would read that Financial Facelift and say “Oh, then therefore me and my spouse will do X, Y, and Z, because the facelift couple did”, and I sincerely doubt that’s the reason for Financial Facelift or for the MoneySense ones, although those tend to be longer. I don’t think that’s the reason that they’re written. They’re written for “economic voyeurism light” in a way.

So yes, it’s to establish the principles, and to say, “Yes, if they think about their TFSA in this way instead of in that way, or if they decide they’re not going to fully fund their child’s RESP”. So there are some good grains of information or ways of thinking. I don’t think they hurt people, to answer that question, but there’s no nuance. I mean, Eric and Ilsa could have been—the story, as written, could have been a reflection of true facts, and much of the nuance that would have made that a legitimate planning problem is lost in the 800 words.

So what if there was—I used this example multiple times already, but what could possibly be the facts that could explain that couple? Not in a way that’s acceptable to me because they don’t need to explain themselves to me, but in a way that would mean, the answer is not just “work one more day a week.” So maybe they have five severely disabled children at home, or they work with charity the rest of the time. So in 800 or 1,000 words, there is no way to talk about the values that this couple have and why this is a particular problem for them. There is really only a set of facts, a planner equation, a solution, and everything is done. On to your next column.

Who’s looking for these facelifts, anyway?

Alexandra: And I think that it’s worth thinking about. You know, we’ve said that this doesn’t hurt the people that receive facelifts, but I think it probably doesn’t help them, either. And there’s two things that I think about why people… So clearly people write in, they want this financial advice, they want the idea that somebody who is perceived as an expert is going to look at their scenario and provide some kind of impartial, professional advice.

So, it tells me that they don’t feel that they’re getting that now, and that to me is a big question about, well why is it that they would feel like The Globe and Mail’s 800 words is worthwhile. If Eric and Ilsa, [laughs] if they were ever, you know, revealed in their community… You know, I wonder about future Financial Facelift people if they’re going to say “I’m not willing to risk the potential worldwide scorning that can be heaped upon me from participating in this”.

But the other part of it, so apart from thinking, “Hey, The Globe and Mail, this 800 words is going to help me”, is the dilemmas that people bring—so I’ve been reading this thing for more than 10 years—are often extremely basic or at least they’re characterized as such in the column.

So people aren’t finding the advice that they think they need, presumably, in their community. But their questions are very basic, so the level of financial literacy seems, that’s to me where I would go to, like, “why do these financial facelifts exist?”

Robb: And your first point kind of leads me to what I found interesting when The Globe, I think they published an article, it was like a letter to the editor, questions to the editor. And it was so why do these kind of 1 percenters get profiled all the time? And so their answer was basically, “well we welcome all types of different profiles; however, we kind of lose people when we want to take your picture or we want to share more details than many people are willing to share. So what we typically end up with is the couple with the defined benefit pension plan and either higher income or a boatload of assets.” And just like you said, maybe they’re not getting that advice in their community and they’re wanting to know how best to optimize this, or can I meet two or three of these goals.

So I thought that was interesting on kind of who writes in, and I believe that. I believe that and maybe it’s about the oversharing that people with what they feel are financial problems or they’re buried in credit card debt, or consolidation loans, or whatever. They don’t want to share that for fear that might get out, or if anyone’s ever read the comments on a Globe and Mail article, you certainly wouldn’t want to be featured in it. [laughs]

Sandi: Do you know, I wonder though—it’s something we’ve talked about before this episode began—I mean, Alexandra, you say you’ve been reading them for 10 years. Do you think that someone with a boatload of credit card debt, instead of a boatload of assets, sees themselves in these columns, or would it even occur to them that they’re in a situation where a little bit of cashflow planning might actually help them?

Alexandra: Yeah, I think that that’s exactly right that you have to think that things are basically okay, to think that a quick, anonymous, third-party review would be helpful. You can’t think things are dire because then you’d seek a different solution.

Sandi: And the the ironic thing about this is the fact that with the asset -level of the typical profilee ,they have access to relatively kind of fee-friendly advice. People with more money tend to have access to better or more full-service planning firms that may or may not also do investing. And for the people who don’t have as much money, as you know, if it’s represented as a percent of their investable assets, it’s way more expensive for them. So I would think that the idea of free, anonymous work with a financial planner would seem more appealing to somebody that doesn’t have access to that.

The screams for accuracy, and how these facelifts actually get made

Jackson: Okay, I want to start talking about the journalistic integrity here, because there is some serious problems with this story, and can we think going forward that there’s even accuracy in any of them? I mean, the outrage! The outrage was there for a reason. For me, I wonder why did this guy write in in the first place? Why is he having financial troubles? I mean they’re making $450K a year, they’ve got no debt except maybe a 2.4% so it’s a variable rate on a lot, at 70%, probably a credit union. There’s a lot of things you can take away from this situation. Why is he having a hard time getting a mortgage? Well, maybe he’s got a professional corporation and he’s writing down his income. There’s probably reasons, but the article just doesn’t get into it.

The facts aren’t there to actually give the full picture and the facts that are there are wrong. How many times did they make mistakes? They made a mistake on how much they made, how many days a week they made, then how many hours a week he worked, then they drew that back down. I mean, you might as well just completely rewrite the article and change the names to other people in Frozen. Have you noticed that by the way? Both Eric and Ilsa are Frozen characters.

Robb: That’s Elsa by the way. I’ve watched it many, many times, as Sandi probably knows too. [laughs] Just a background on the income versus expenses. So for anyone who didn’t read that article, they made $25K a month, and they spent $31K.

Jackson: Robb, just let that sit in.

Robb: Yeah, $25K.

Jackson: $25K a month, working one day a week.

Robb: And they spent $31K a month, right? So the first error was that in the expenses there was a huge mistake and that was that they somehow spent $6K a month on professional fees and dues, and that turned out to be $6K a year. So, they talked about in the article was this gap of $5K a month. Well, there it is, right? And so, that changed the story completely. Just with that one error, and let alone you need to work one more day a week, but actually no, you work 100 hours a week.

Jackson: Yeah, the advice was “Work another day a week” or go into debt and borrow a million dollars from your parents until your kids are in college.

Sandi: We’re talking about two different things. You’re getting angry because they’re rich and 1%, Jackson. But let’s go back for one second. Let’s talk about this idea of accuracy, because these people are not submitting their actual statements of assets and liabilities. It’s a two page form. I’ve seen them, and Alexandra, obviously you’ve seen them. They have to self-report their expenses and then they’re assets, and the name their top three concerns, or whatever. Again, it’s two pages, so the author of the report, and I imagine—for more than just The Globe and Mail—it’s not a fact-checking situation, and I don’t fault them for that. I don’t think it should have to be, but it is a logic situation.

Alexandra: But you know, people kept calling on Twitter for it, “This needs to be fact checked.” And I think to myself, well what is it that the journalist is supposed to do? Is she supposed to confirm that these are living, breathing people?

Sandi: Well if we have to fact-check, that means that the article is meant to serve the people reading it more than it’s meant to serve the people who are self-reporting their income. Like if that’s what they say they make, and that’s what they say that they pay in expenses, then they’re the ones that are hurt if there’s any inaccuracy, right?

Alexandra: Well I can really see how this happened. I mean, as a physician if he says I have one clinic day and one teaching day. Maybe the planner looks at that and says, “Oh, two days”, versus going back and saying…”right, what does one clinic day mean? How many hours a week do you work?” It seems clear from what was published that step of going back and asking the facelifted person about how many hours were worked wasn’t done and obviously the guy wrote in afterwards and said “No, no, no, I work 80 hours a week”.

Robb: So does the article get published with the planner’s advice before anything goes back to the submitter of the information to say “Oh okay, well that’s cool. I’ll work one more day a week then”?

Alexandra: I’m not aware in the two that I did, I’m not aware that they went back. I mean, I think that what happens is this person opens up the newspaper and says, “Oh look, there’s my scenario.”

Robb: Okay.

Sandi: And look there’s my parody of a Twitter account. [laughs]

How these facelifts should get made

Alexandra: So I, you know, I was talking to Sandi earlier about in an ideal world, how would this happen? And you know, I think there’d be like a committee, maybe a committee of planners, who would look at this scenario and would say okay and what do we need to check out. What do we need to verify and then what are the strategies we’d want to propose? And that is a very different proposition than 600 words banged out between Tuesday and Friday.

Robb: Right. And like you said, I can totally see how this would happen. So I’ve had clients that will submit a form back to me, but because they pay their mortgage two times a month, or biweekly, and I’m asking for what’s your monthly mortgage payment, they don’t actually do that math to convert it into a monthly.

So even if that’s $100, it skews the numbers and the accuracy that I can give for advice, right? And so I’m sure you’ve dealt with that Sandi. And you’ve complained before about when you self-report the numbers and you’re not actually tracking properly your expenses, and you have these round numbers of, “I spend exactly $1,000 a month on groceries”, you know what I mean?

So I can definitely see how those numbers don’t have to be accurate, but you could see right in the initial comments, there was a surgeon that came up and there’s like, “There’s no way he’s doing that for one day a week”. So the readers all caught on and I think that was the big “gotcha” moment. It wasn’t for the readers, it wasn’t the monthly payments are out of whack, or whatever. It was like you guys missed the boat here.

Alexandra: Well it was fascinating to me that they kept changing the disclaimer at the bottom, “Here, we’re issuing a clarification”, and yet the advice remained the same. So clearly the advice no longer is suitable, right? He can’t work one more day a week if he’s working 100 hours a week, or 80 hours a week even. So it just was so unsatisfying for readers, unless you love the Tweets, right?

Jackson: Oh, it was very satisfying for quite a few people. [laughs]

What does the Globe and Mail care about, then?

Robb: Yeah, just satisfying for that end for sure. And I think that kind of goes back to my earlier comment about well what does The Globe and Mail care about here? Is it all the eyeballs on this story? And I think if you change that story then you lose all those residual clicks that are going to come from when the Gawkers of the world pick it up, and that sort of thing. So they can make a little footnote on the bottom, which to us reading it, we think that’s ridiculous. You need to change the whole story. But I think they want the eyeballs on that original story to say this is what the outrage was about and then here’s our little footnote at the bottom.

Alexandra: But it’s interesting that there’s a whole level of journalistic outrage. So what I see in the Twitter stream is people saying the public editor of The Globe and Mail needs to be called to account for this. Like it’s totally separate from the advice side of it. You can’t publish things that you haven’t verified.

Robb: Well it seems very tabloid-like right? You know, in the way that they lured in this other whole audience when it blew up on Twitter, and even when some US sites picked it up. You know, that’s when it seemed so sensationalist.

Alexandra: Well I’m very curious to see the Financial Facelifts going forward. I wonder if people who are scheduled to be profiled are now going to say, you know what, it’s not working out. [laughs]

Robb: There’s no way. So would you do another one as the planner?

Alexandra: Well it’s a good question. I wonder. You know, the reason that I got invited to do one in the first place was I had a friend who wanted a facelift and who is one of the people who backed out because of her concern that she was going to be identified. That just because her scenario was so unique, and whatever, that they weren’t going to adequately mask her identity. And she’s like, “Ah, I don’t want to do it”. But then the journalist asked me if I would be interested in doing one, and the scenario was so unusual with this elderly woman’s scenario, and I thought, “Oh this is actually kind of an interesting puzzle to think about”, like my creative juices started flowing. So it was really I just fell into it with no particular plan to ever do a second one or a third one.

Robb: Sure.

Alexandra: So there’s a non-answer for you. [laughs]

So are we all just made at Eric and Ilsa for being rich, or is it something else?

Robb: Jackson, I think we’re close to our time here, but I want to hear at some of the—like this blew up. I mean, I think it comes out on Saturdays and I didn’t see it on the Saturday, but the Sunday, Monday it was going crazy on Twitter and other blogs were picking it up. But there was some wild stuff before the facts got repurposed, or got checked. Jackson, what were some of your favourites when you were following on Eric and Ilsa’s hashtag.

Jackson: There’s a ton of them. The Eric and Ilsa account is awesome. I mean, “breaking the Bank of Canada forecast is really messing with Eric and Ilsa’s reno plans”, “More money, more problems, and why high earners sometimes struggle just to pay the bills”. People are writing blogs about this. They’re making memes. “I think our work here is done. Would love to hand off this Twitter account to a Canadian charity startup.”

So I mean, there’s some things that are going on. I mean, this happened when, last Friday? It’s now what, a Wednesday, and it’s still very active. On Twitter, it’s hourly updates. I think one of my favourites was that people are saying, “Oh that’s Eric and Ilsa money”. Like that’s becoming the top dog for money now, like, “Oh, Eric and Ilsa money”, you know, cash money baby.

To me it really worked. I don’t think it was people getting around and making fun of the 1%. I really think that misses the mark. I think it was just kind of like, you have got to be kidding me. You know, come on, it’s not about the 1%. I think it was about the bad journalism on this one particular story, and I think people had fun with it. And I don’t begrudge them because I was kind of cheerleading.

Robb: One last question, Alexandra. So, we’re talking about the 1% and in the last couple years it’s been this—what do they call it, the “YOLO” mentality, you only live once. And so all the conversation that happened about Eric and Ilsa, and maybe it is about the 1%—who knows. You know, when you dig deep down, is this a way that we now started a conversation to say, well it’s not really okay to YOLO your way through life?

Sandi: Isn’t that always the conversation? I would hope that that’s a quiet conversation that’s always happening, when sensible financial planning. I mean, when sensible financial planners are looking at their clients and saying, “Let’s talk about. Let’s lay your investments aside” — it’s going to be the same old story from Sandi Martin, but– “how do you spend your money every single day, every single week, every single month, every single year. Let’s talk about that and then let’s talk about what you want to do with that and only then how you’re going to invest and what house you’re going to build, etcetera.”

Alexandra: Well I think that Eric and Ilsa, whoever they may actually be and whatever their scenario might actually be, are genuinely in need of a plan, right? They could genuinely benefit from some financial planning. I think though, as physicians, there’s a human capital story there which makes them quite different. You know, I have no idea what the details of their scenario are, but he could be a radiologist with huge earning potential. Dentists, you know, their scenario is different from salaried employees who have a fairly non-volatile, stable source of income. The amount of debt they’re in may be completely logical. Depending on their stage of life and their other financial commitments, they could easily afford a million dollar house and even the lifestyle they want. This is about consumption-smoothing, right? This is a different conversation than fixing up one piece of their finances now. I’d like to take a look at the whole lifecycle for them and plot out what’s the optimal path for them to spend over their lifetime. You’re smiling at me there, Sandi.

Sandi: Because I like hearing all those words. [laughs]

Alexandra: I’m just saying that it’s you know… I said earlier that it seems to me that readers want people in these facelifts to be spanked, but I think that even situations that can look unusual from the outside may not be spank-worthy, but with this particular case, it’s pretty much impossible to say.

Sandi: That’s the thing. You know what? Let’s go back then to the fact that it’s 800 words and these are people who we don’t know. As much as we want to look at the few brief facts about their life and say, you’re a total waste of space and how dare you clutter up my British Columbia with your snobbiness, they’re people. They genuinely looked for help. Maybe they are misguided, maybe they’re making some poor choices, but there’s no possible way, and I think The Globe and Mail is perpetuating this, if indeed this is kind of 1% voyeurism, The Globe and Mail and the Financial Facelift kind of trend, or whatever you want to call it, is perpetuating this feeling of “let’s just look at their details and judge them based on that and not worry about them being real people.”

Alexandra: Well, The Globe is providing the window. We’re just merely looking through it, right?

Robb: And we drew our own conclusions with this one, I think.

Jackson: And I’m going to leave with a quote from Kerry K Taylor at Squawk Box, “I’m trying to keep up with Eric and Ilsa lifestyle, but the hilarious story of corrections are distracting me from work.” I think she nails it there.

And I think we’re out. Good-bye.

Sandi Martin

Sandi Martin

Owner

Because Money Ep 26 | Eric and Ilsa

Source: http://www.becausemoney.ca